In modern commerce, payments have largely followed the same pattern. A person decides to buy something, a merchant charges them, and the financial system settles the transaction afterward. Credit cards, online checkout, subscriptions, and mobile wallets have greatly reduced friction in that process, but they have not fundamentally changed who is in control. The human has always remained the decision maker at the center of the transaction.

AI agents change that model. As AI moves from generating content to executing actions, agents will increasingly search, negotiate, procure, and transact autonomously. In this new paradigm, payments cannot solely remain a human-triggered event. They must move inside the execution layer itself, integrated directly into the workflows and tasks agents carry out.

Agentic payments are the systems and tools that make this possible, enabling agents to initiate, authorize, and complete financial transactions as part of autonomous workflows. Not only is this an evolution of how value is exchanged for goods and services, but it is a fundamental expansion of who or what can participate.

Our view is that agents will drive a growing share of economic activity across digital and physical commerce. By 2030, agentic commerce could drive up to $17.5 trillion in commerce according to Deloitte. As this shift unfolds, a new financial paradigm is emerging: one in which agents become economic actors, equipped with native payment capabilities to allow them to transact autonomously.

From Human Commerce to Autonomous Execution

Commerce is evolving through a sequence that is familiar across many technology cycles.

Initially, humans transacted directly with each other. Eventually, software embedded payments inside applications and digital products. Now, agents are becoming the actors that decide when and how transactions occur.

That shift creates three distinct emerging payment flows:

- Human-to-agent. A person delegates authority to an agent within defined constraints. For example, an AI assistant books travel within a budget, renews subscriptions, or completes routine purchases on a user’s behalf. In these cases the core challenge is safe delegation, where systems must determine who authorized the action, what spending limits apply, and where liability sits when software acts on behalf of a user.

- Agent-to-business. Agents interact directly with merchants, vendors, or APIs without a human involved in the transaction itself. This could be an AI agent purchasing compute from a cloud provider, paying for an API request, or ordering supplies within an enterprise procurement system. In these cases payments become part of the operational workflow rather than a checkout step.

- Agent-to-agent. Autonomous systems negotiate, purchase, and settle with other systems directly. This may look like a marketplace of AI services that bid for tasks, supply chain systems that automatically restock inventory across vendors, or merchant-side agents that dynamically negotiate pricing with buyer agents.

Across all three payment flows the pattern is the same: software is no longer recommending actions, but executing them.

A New Protocol Layer Is Emerging

As agents become the decision makers in transactions, identity, permissions, and payments cannot remain buried inside application logic. They need to become standardized and machine-readable components of the ecosystem.

The strongest signal that this shift is real is that major platforms are already moving swiftly to operationalize pieces of the stack. Preparing for a world in which transactions originate from agents rather than humans.

The strongest signal that this shift is real is that major platforms are already moving swiftly to operationalize pieces of the stack.

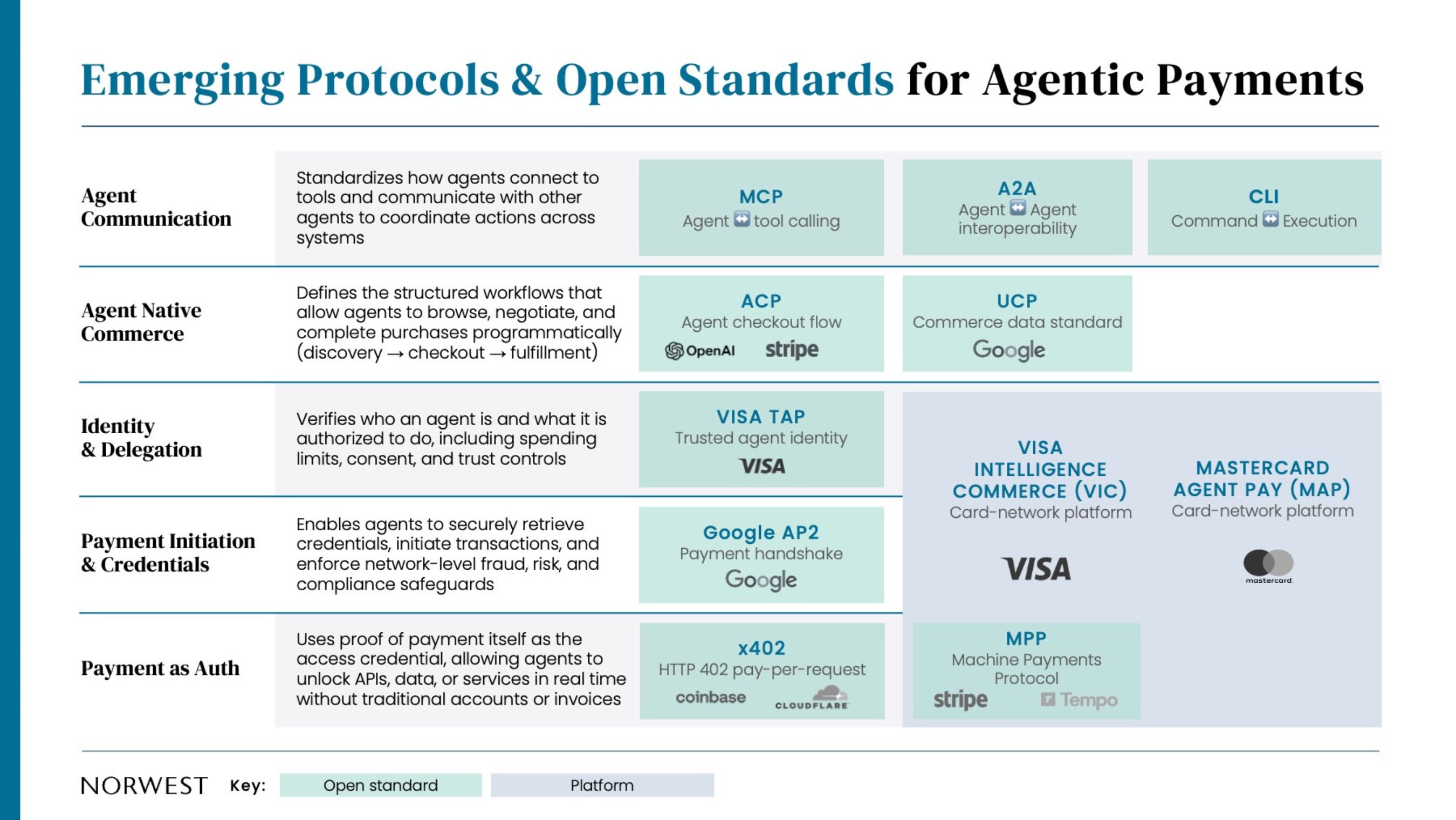

Standards such as Anthropic’s Model Context Protocol (MCP) and Google’s Agent2Agent Protocol (A2A), along with command line interfaces (CLIs) allow agents to invoke tools and coordinate actions across systems.

Commerce schemas such as the Agentic Commerce Protocol (ACP), developed by OpenAI and Stripe, and Google’s Universal Commerce Platform (UCP) structure how agents browse, negotiate, and complete purchases programmatically. Identity frameworks like Visa’s Trusted Agent Protocol (TAP) focus on verifying who an agent represents and what it is authorized to do.

Payment infrastructure is evolving as well. Google’s Agent Payments Protocol (AP2) initiative introduces machine-native payment handshakes between services. Visa Intelligence Commerce and Mastercard Agent Pay aim to extend card network infrastructure into agent-driven environments. Meanwhile, Coinbase’s x402 proposal and Stripe/Tempo’s Machine Payments Protocol (MPP) explore a model where payment itself becomes the authentication credential that unlocks services.

The casual observer might get dizzy from the alphabet soup that defines this early, fragile stage of a new market. Taken together, though, these efforts suggest that payments, identity, and service access are converging into broadly adopted shared protocols for machine commerce.

When Requests Become Transactions

Today, most digital commerce separates product usage from payment settlement. Systems meter activity, aggregate the data into invoices or subscriptions, then bill and settle the payments later as a distinct financial event. A traditional card swipe works pretty well in this model, but agent-driven systems may push toward a different structure.

One likely evolution of agentic payments is the collapse of billing and payment into a single primitive. Instead of handling payment as a separate step, the request itself carries the payment authorization needed for execution. An agent requests a resource or service, includes proof of payment as authorization, and the service executes as soon as that payment is verified.

One likely evolution of agentic payments is the collapse of billing and payment into a single primitive. Instead of handling payment as a separate step, the request itself carries the payment authorization needed for execution.

Execution and payment effectively happen together.

Some early initiatives already hint at this direction. The x402 proposal uses proof of payment as a credential that unlocks an API or dataset in real time. Instead of authenticating with an API key, the request itself carries a payment signal that authorizes access. MPP, operates in a similar fashion: an agent can request a resource from a service, API, MCP, or any other HTTP endpoint, receive a payment request in response, authorize it, and unlock access in real time.

In both examples, an internet-native currency like a stablecoin could be a convenient payment method, especially for micropayments where minimum card fees may make the transaction prohibitively expensive. As we noted in our Fintech 3.0 post, we are excited about the power and programmability of stablecoins and see their application to agentic payments as a natural extension of their role as the internet’s native currency.

That said, we think traditional cards and stablecoins will both play an important role in the new agent economy. In fact, one of the more interesting announcements of MPP was Visa’s related card-based spec that extends MPP to support card-based payments as well.

Where New Agentic Payment Companies May Emerge

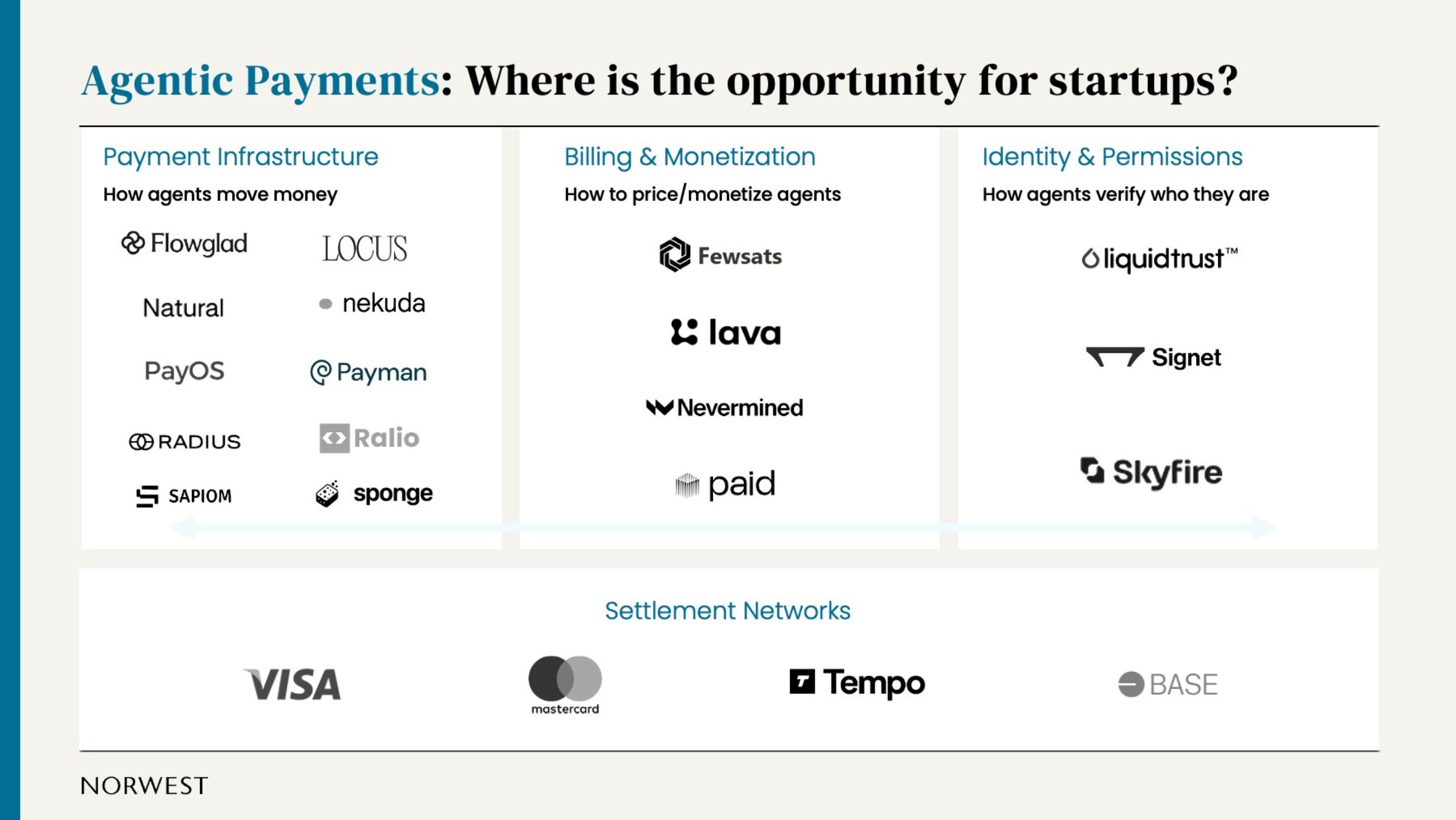

As agents begin to transact autonomously, we see a new ecosystem forming across three categories today:

The first is payment infrastructure. These systems handle the wallets, routing, settlement, and execution primitives that equip agents with the tools to move money and enable merchants to accept agent-initiated payments.

The second is billing and monetization. Before agents can transact broadly, businesses need a way to understand what agents cost, how value is created, and how to capture margin. Systems that provide real-time usage metering, cost attribution, pricing, invoicing, and spend controls will give companies the confidence to deploy agents more autonomously.

The third is identity and permissions. Agents need a way to prove who they represent and what they are authorized to do. Systems that manage delegation, authentication, and spending limits will become foundational for machine commerce.

In practice the boundaries between these layers may blur. Money movement, pricing, identity, and execution logic may increasingly converge into unified platforms designed for autonomous systems.

The Next Phase of Digital Commerce

Many financial interactions will still look familiar in the near term. Subscriptions will renew. APIs will charge for usage. Vendors will receive payments. Inventory will be reordered.

But as agents become economic actors, payments stop being the end of a transaction and become part of the execution itself. Behind the scenes, the actor making those decisions will increasingly be an agent rather than a person. Wallet balances may replace invoices in some workflows while identity and authorization may become machine-verifiable.

Payments may occur inside service requests rather than after the fact. That shift will force payment networks, processors, and merchants to rethink fraud models, identity frameworks, and operating rules for a world where agents participate directly in the economy.

As these new payment flows grow, we believe significant value will accrue to the startups building the infrastructure, control layers, and workflows that make agentic commerce possible. We’re excited to see how the ecosystem evolves.

If you’re building in the space or have any thoughts on the agentic payments ecosystem, we’d love to chat! Reach out to us: Jordan Leites (LinkedIn or email) or Nikhil Goel (LinkedIn or email).